Energy, Politics & Money - 18 December 2022

Energy, Politics & Money - 18 December 2022

Independent, objective, and politically neutral analysis of interconnected global developments in the world of energy, geopolitics, and money curated to help you thrive or survive these chaotic times.

In this roundup, EPM takes a closer look at what Germany has been doing to keep the lights on amidst its energy crisis. Since the start of the Ukraine War it has spent about € 1.5 billion - half a trillion dollars in total - on energy (and growing). In EPM’s view this should make abundantly clear that Europe is staring at an economic crash in 2023 and something much worse than ‘just’ a deep and long recession. It has created for itself an energy crisis that will devastate its industrial base with one consequence being further damage to an economy that is already severely affected by inflation and resulting tightening of monetary policy.

If you don’t have time to read today’s column right away, here are some main points included in today’s roundup, we look at:

The shipments of Russian crude oil to India, on tankers insured by western companies, which is an indicating Moscow might be reneging on its vow to block sales under the G7-imposed price cap

Chinese crude oil stock building, which has lifted crude oil demand, supporting the OPEC+ view that the market is not in a state that supports a quota increase

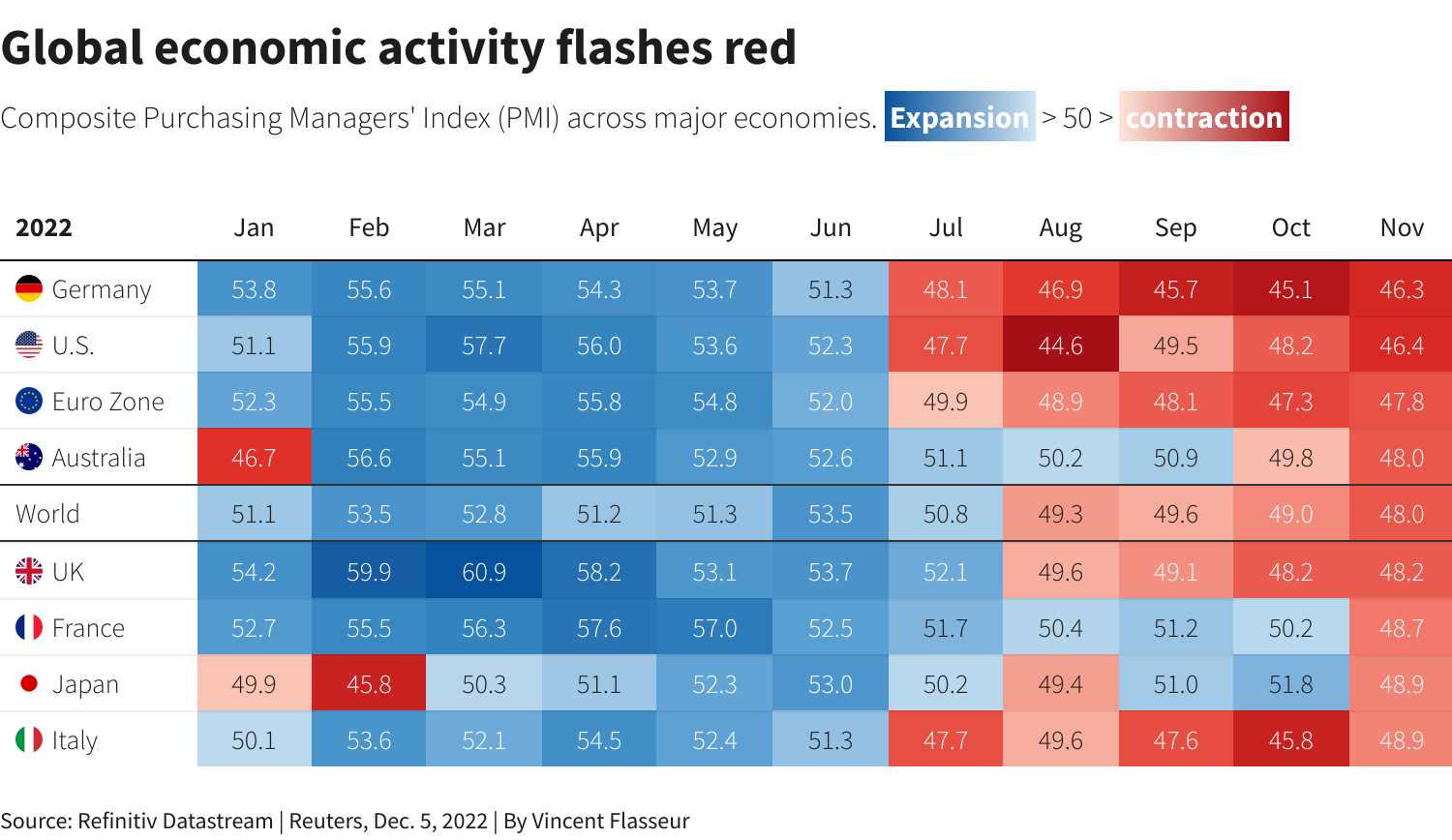

The dramatic decline in the Purchasing Manager Index in all the world’s leading economies

The latest US move to tighten the thumbscrews on China when it comes to the semiconductor industry

The Idemitsu expectation that cleaner fuels such as ammonia, green pellets and sustainable aviation fuel (SAF) will not contribute to its profits until 2030

The outlook for electric vehicles, as a wave of new electric vehicles from pickup trucks to middle market SUVs and sedans will hit the world’s major markets, while the global economy is entering a recession, causing new vehicle sales to decline rapidly

General Energy News

Russian crude oil is being shipped to India on tankers insured by western companies is the first sign Moscow reneged on its vow to block sales under the G7-imposed price cap writes the Financial Times.

Reports earlier this week indicated that the true state of crude oil demand has been masked over recent months for example by the disruptions caused by sanctions on Russia. Clyde Russel at Reuters reports on another “mask” namely Chinese crude oil demand. China does not disclose the volumes of crude flowing into or out of strategic and commercial stockpiles, but an estimate can be made by deducting the amount of crude processed from the total of crude available from imports and domestic output. Over the first 11 months of 2022 the volume of crude going into inventories was around 700,000 bpd. This of course means that Chinese stock building has lifted crude oil demand – supporting OPEC+’s view that the market is not in a state that supports a quota increase.

Bloomberg reports that Chinese crude oil demand faces a bumpy road to recovery. Post Zero COVID, the spread of the virus will first cause continued disruption of the economy, and only start to enable recovery in 3 to 4 months’ time – indeed, exactly as EPM forewarned earlier.

Macroeconomics

The US Fed raised its benchmark rate by 50 basis points this week, exactly as expected. But, Bloomberg reports, Chair Jerome Powell said it is not close to ending its anti-inflation campaign of interest-rate increases. “Restoring price stability will likely require maintaining a restrictive policy stance for some time” he said.

The ECB followed the Fed and also raised rates by 0.5%, while similarly indicating more rate raises should be expected in 2023 writes the Financial Times. ECB president Christine Lagarde said the bank had “more ground to cover … longer to go” than the Fed.

Meanwhile, Reuters reports on the Purchasing Manager Index (PMI) across the world’s major economies. It is deep, deep red, which in our view at EPM should convince anyone who is not convinced yet, that a deep and long recession in underway.

Japan’s manufacturing activity shrank at the fastest pace in more than two years in December writes Reuters and is explained by weak demand.

Geopolitics

In another move that increases tensions between the US and China, the Biden administration has added a further 36 Chinese companies and research organizations to its trade blacklist writes Nikkei Asia. Top Chinese companies such as Huawei and its top chipmaker Semiconductor Manufacturing International Company were already on the trade blacklist. Yangtze Memory Technologies Company, China’s top memory chip producer, and Shanghai Micro Electronics Equipment (Group) Company, which represents the country's effort to build a local version of leading lithography chipmaking equipment maker ASML of the Netherlands, were now added.

Energy Transition & Technology News

Idemitsu, Japan's number 2 oil refiner, expects cleaner fuels such as ammonia, green pellets and sustainable aviation fuel (SAF) to contribute to its profits by 2030 writes Reuters. Idemitsu is changing its portfolio by scaling down fossil fuel assets while investing in greener energy and battery metals, but it doesn’t see these demand for these products reaching the level that is needed to make a profit over coming years.

The Electrification of Transport

Reuters writes that 2023 is set to be a critical year for the electric vehicle industry. A wave of new electric vehicles from pickup trucks to middle market SUVs and sedans will hit the world’s major markets. The key question will be whether consumers can be convinced to make the switch on a mass scale. EPM’s view is that EVs are exiting the stage where early adopters made up the majority of customers. This segment of the market is intrigued by innovation and therefore not primarily focused on cost analysis. The next segment of the market will need to be convinced by brand, convenience, comfort, and price and therefore requires a different marketing approach. EVs are clear winners in all these categories, except price and, to a lesser degree, charging comfort. The biggest challenge we believe will be, therefore that this critical moment for the industry is coming in the midst of a global recession. As highlighted by Paul Hodges over at New Normal, this is causing a rapid decline in new car sales. How will this play out? EPM expects the share of EVs in new car sales to be solid, but absolute sales volumes to disappoint. This will prove the mass appeal of EVs, but disappoint investors, who will need to wait a few years, until the global recession is over, to see volumes pick up.

The Global Energy Crisis

At EPM we said from the very beginning of the energy crisis in Europe, that sovereign efforts to manage the cost impact for households and industries would quickly turn out to be unaffordable – i.e. a dead end rather than a real solution. Reuters reports that Germany is bleeding cash to keep everyone’s lights on. It has already spent almost half a trillion dollars since the start of the Ukraine War, about €1.5 billion a day. In EPM’s view this should make it abundantly clear that Europe is staring at an economic crash in 2023, something worse than a deep and long recession. It has created for itself an energy crisis that will devastate its industrial base the consequences of which will be further damage to an economy already severely affected by inflation and the resulting tightening of monetary policy.