Energy, Politics & Money - 12 August 2022

Energy, Politics & Money - 12 August 2022

Curated news from the ever evolving worlds of energy, geopolitics, and money just for you!

Welcome to the Energy, Politics & Money news feed of Friday 12 August 2022, with your daily dose of cutting-edge insight into everything of importance in the connected worlds of energy, geopolitics and the economy.

In this roundup, we:

Take a deeper look at factors driving oil prices

Examine the risk of tightening monetary policy on zombie firms - it doesn’t look good

Review world wide EV adoption

How U.S. EV manufacturers won’t benefit from Biden’s new energy bill

EV’s reduced a Japanese firm’s cost by 30%

Hydrogen fuels are not quite dead yet if BMW and Toyota have anything to say about it

Europe’s strategic gas supply comes at a big cost.

General Energy News

As highlighted in previous editions, Wednesday was an important day for the short-term oil price outlook as both OPEC and the IEA released their monthly outlooks. We predicted that since market sentiment was already negative (due primarily to economic growth concerns), if their reports did not contain analysis supporting crude oil prices, the downward trend of the oil price we’ve seen over the past few weeks would likely continue for the coming weeks. Reuters of analyzed both reports. As to the OPEC’s monthly report, it was primarily negative as it focused on the impact of lower economic growth on oil demand. It trimmed its 2022 global economic growth forecast to 3.1% from 3.5%, expecting 2022 oil demand to rise by 3.1 million barrels per day (bpd), or 3.2%, down 260,000 bpd from the previous forecast. As for the IEA’s monthly report, it too raised concerns about the economic outlook but it contained grains of analysis supporting the oil price. It highlighted that the global energy crisis is primarily due to shortages of natural gas and that this is driving the switch from gas to oil-derivatives supporting crude oil price. The IEA in response to its optimistic view of the oil consumption, raised its 2022 demand increase outlook by 380,000 barrels per day for a total increase of 2.1 million barrels per day.

As was to be expected, therefore, oil prices dropped in Asia during early trading on Friday as the uncertain demand outlook continues to dominate trader sentiment. Reuters reported Brent futures fell by 49 cents (or 0.5%) to $99.11 a barrel at 0330 GMT, while WTI crude futures fell 50 cents (or 0.5%) to $93.84 a barrel. But, Reuters highlights, while this has happened almost every day this week, oil prices have tended to strengthen during later day trading setting crude oil prices up for a modest weekly gain of 4% this week compared to the 14% drop last week. This is also what Bloomberg focuses on in its review of the oil price movements this week.

Further to the IEA’s monthly market report The Guardian highlights it included a discussion of Russian oil production and exports. Apparently, according to the IEA, Russia’s oil production in July was 310,000 barrels a day below prewar levels while total oil exports were down by about 580,000 barrels a day. Meaning, the main effect of U.S. and European sanctions has been the redirection of Russian crude oil supplies from Europe to India, China, Turkey and others. The IEA also says the EU embargo on Russian crude and product imports - which comes into full effect in February 2023 - will result in further declines.

A few days ago we reported on ExxonMobil’s planned exit from onshore operations in Nigeria. The Financial Times reports that this plan is now in doubt as the Nigerian president suddenly and unexpectedly withdrew his support for the sale less than three days after approving it.

The Macro Environment (economics & geopolitics)

Deutsche Welle has taken a look at so called “zombie firms” in the economy, and how these are likely to be affected by the monetary tightening that is taking place around the world. The report is an opportunity for us to explain more why we believe current monetary policy will have a severely negative effect on the global economy:

Monetary tightening always leads to economic slowdown (based on historical data). In fact, that is what it is precisely intended to do;

The current period of monetary tightening follows an extended period of unprecedented loose monetary policy during which money was available at zero or even negative interest rates. Naturally, such a period of loose monetary policy creates bubbles in the economies (clearly visible in the real estate and the stock markets); and,

Central banks around the world have been late in recognizing the “stickiness” of the current inflation, they will recognize they have to hit the break harder and faster to bring it down to acceptable levels. This creates an abrupt shock to the economy that worsens the impact of the monetary tightening.

As the Deutsche Welle report explains, loose monetary policies enabled inefficient and unprofitable firms to operate in many sectors and remain afloat that otherwise would have gone bankrupt due to unsustainable operations or business models. We predict, therefore, that this period of monetary tightening will have an even bigger effect on the economy than a typical period of monetary tightening - many bubbles are at risk of bursting because they were inflated over the 2008 – 2022 period.

An opinion piece in Bloomberg uses the Bank of England’s plan to raise rates and to simultaneously reduce its loans outstanding by $100 billion, to argue the same point: this degree of rapid tightening is likely to severely affect the economy.

Transport Electrification

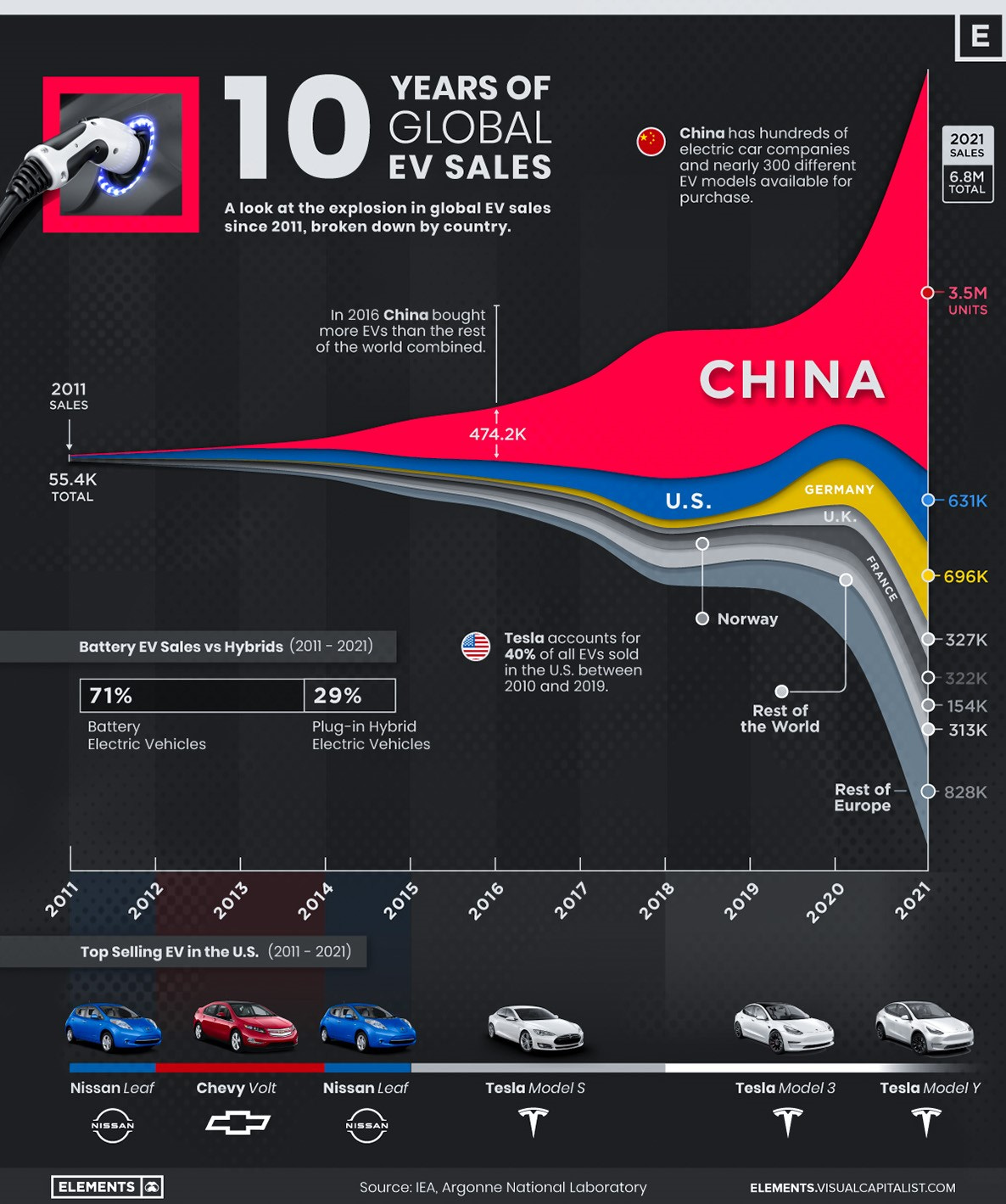

Visual Capitalist has looked at 10 years of global EV sales and translated it into a wonderful info graphic. Please note the S-curve development. In case you are wondering whether this will lead to, the article “Wake up call for oil companies: electric vehicles will deflate oil demand” from 2016 modeled EV penetration and its impact on oil demand using a S-curve approach (unlike conventional forecasts which, contrary to real world circumstances, tend to apply constant growth rates).

Meanwhile, Reuters reports that Rivian confirmed that many of its current EV models will not qualify for the new federal tax incentives included in the energy and climate bill passed by the U.S. Senate. We identified this risk last week by highlighting that the bill limits incentives only to EVs that utilize a domestic battery supply chain and therefore many of the cars currently manufactured and on sale in the U.S. won’t qualify.

Over in Asia, Nikkei Asia carries a report confirming one of the pillars underlying our bullish outlook for the electrification of transportation, namely that as battery technology matures it will enable significantly lower cost of transportation and greatly increase demand for electric transportation solutions. Nikkei Asia’s report is on SBS Holdings, a Japanese logistics company, which found that by buying electric vans assembled in China it lowered its operating costs by 30%.

Nikkei Asia also reports that BMW has announced it will start mass-producing and selling hydrogen fuel cell vehicles it has developed jointly with Toyota Motor “as early as 2025”. We would have said, “as late as 2025” ;-) Our view is that by 2025 the penetration of battery electric vehicles will have progressed significantly, as will the build out of the infrastructure in homes, at malls, and along highways that are needed to support them. This, we believe, will prove to be an additional hurdle for Fuel Cell Vehicles to become mainstream.

The Global Energy Crisis

Reuters has a deep dive on Europe’s natural gas inventories. The good news is that European gas storage levels surpassed 70% at the start of August, in line with their average over the 2017-2021 period, according to data from Gas Infrastructure Europe (GIE). The bad news is that this is being achieved by (i) cutting back on use, (ii) switching from gas to coal, and (iii) importing additional LNG that would under normal circumstances go to Asia by offering record prices.

Bloomberg reports that Japan and South Korea are also rushing to secure supply for winter, which of course exacerbates the global LNG shortage and will drive prices higher leaving poorer countries in Asia, such as Pakistan and Bangladesh, without access to the fuel.