Energy, Politics & Money - 07 November 2022

Energy, Politics & Money - 07 November 2022

Independent analysis of interconnected global developments in the world of energy, geopolitics, and money curated to help you thrive in chaotic times!

In this roundup, we look at the shorter-term outlook for the crude oil price. It settled up significantly higher for the week last Friday, Brent at $99 per barrel for a weekly gain of 3%, and WTI at $93 for a 5% weekly gain. Driving the price is not the OPEC+ cut – which is no longer being talked about because of its negligable impact (exactly as we at EPM forecasted). The driver is the disruption likely to be cause by the next round of sanctions on Russian crude oil, including the US’s price cap, coming early December – which we also forecasted.

Meanwhile, on the demand side, demand destruction resulting from the poor macro-economic environment is becoming ever more noticeable, while China over the weekend committed itself (again) to (Net) Zero Covid, leading some to say that the disruption of Russian crude oil flows might end up being a welcome relief for a crude oil price battling downward pressures!

Furthermore, we look at:

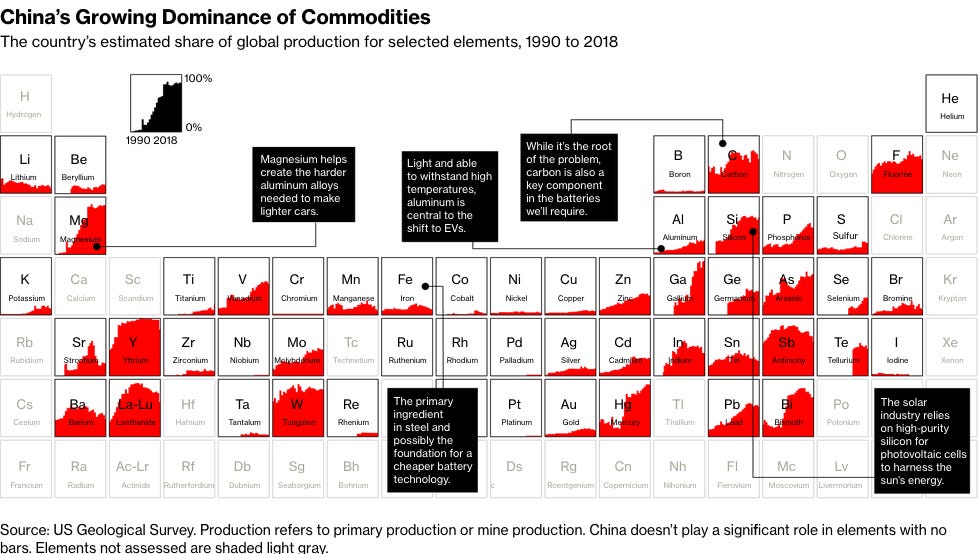

How in the global race for the commodities that underpin a switch to a greener economy, China has become the dominant supplier or processor

The trajectory of the US – China conflict, which is clearly war, as the US pushes its allies to cut China off from semiconductors, the red blood cells of the global economy, while its allies line up to form all sorts of military alliances against China, and its military leaders explicitly forewarn about a coming war over Taiwan

Shell’s investigation of opportunities to do industrial-level CCS in China, including the export of captured CO2 to storage locations internationally

AP Møller-Maersk’s head on assault of the oil industry, which it accuses of not offering sufficient volumes of green fuel – which at EPM we see as an attempt to deflect blame for not delivering upon (much hyped) decarbonization targets

The calls for new decarbonization policies from The Economist, which argues the 1.5 degrees scenario is now unattainable; and on the topic of the new policies, the US plan for companies to fund emerging nations’ fossil fuel switch, which we at EPM believe would remove most of the incentive for companies to work on decarbonization, placing the onus (and associated financial risks) squarely in the lap of governments

The mass protests in Italy against the war in Ukraine, in particular Italian military support to Kyiv, which raises the question how much of existing policies regarding Ukraine and Russia the new Italian government will be able to continue

A review of the history of ESG, where we at EPM ask, are companies which sincerely take ESG on board really making a (noticeably) more positive difference in the societies in which they operate?

General Energy News

The crude oil price settled up significantly higher for the week last Friday. Brent crude futures ended the week at $98.57 per barrel, a weekly gain of 2.9%, and WTI closed at $92.61, a 4.7% weekly gain. The trader sentiment driving the increase focuses on the outlook for demand, and linked to that China’s covid policy and the next steps in monetary policy around the world, as well as the disruptions likely to result from the next round of sanctions on Russia, including the G7 price cap, writes Reuters. At EPM we note that the OPEC+ quota cut has dropped off the radarscreen of traders in the market – exactly as we said it would, as it hardly affects crude oil exports from the OPEC+ countries.

Driving the oil price in early trading on Monday morning is China’s covid policy. Reuters reports the price fell more than $1 a barrel, after Chinese officials on the weekend reiterated their commitment to a strict COVID containment approach, dashing hopes of an oil demand rebound at the world's top crude importer.

Just a month before the G7 cap the price of Russian oil, officials are still racing to finalize details of the program, writes Reuters. This leaves traders, shippers and insurers with questions about the price level and how it will work, and is another way in which we at EPM believe it will cause significant disruption of global crude oil flows – in addition to the retaliations by Russia and the disruption of the derivatives markets we discussed last week.

According to Julian Lee at Bloomberg, with the downward pressures on crude oil demand resulting from the poor macro-economic environment and China’s covid policy, a proper disruption of Russian crude oil flows might be exactly what the markets need to prevent the crude oil price from dropping. To balance supply and demand, the world will need 29 million barrels a day of crude from the members of the Organization of Petroleum Exporting Countries in coming months, even with the loss of 1 million barrels a day of Russian supply from December. With a modest recovery in Nigerian production, which is already underway, that’s almost exactly what the group’s likely to pump if its members don’t exceed their new targets. If Russian supply doesn’t fall, the crude market looks oversupplied in the coming months.

Macro-Economics

The US Fed’s policy of monetary tightening is starting to leave its mark on the US housing market, reports Bloomberg. The surge in borrowing costs has eroded affordability for buyers, slowing residential sales and building activity, and threatening economic growth.

Geopolitics

The US appears ready to pressure Japan and the Netherlands even more to join efforts to block the flow of advanced chip technology to China, writes Nikkei Asia. “I think you will see Japan and Netherlands follow our lead”, Commerce Secretary Gina Raimondo said during an interview. This most likely concerns the semiconductor equipment industry, in which ASML of the Netherlands and Japan’s Tokyo Electron play critical roles. In response, at EPM we repeat that our base case outlook is a regionalization of the global economy into a “western bloc” led by the US, and an “eastern bloc” consisting primarily of China and Russia. Companies in most industries will be forced by regulation to choose a bloc to play in, with “playing in both” no longer being an option. In light of this outlook, which EPM believes is obvious for those with an open mind, we wonder what the thinking was behind Germany’s chancellor Olaf Scholz visit to China last week? Surely, he must see the above writing on the wall? If he wants Germany to continue doing business with China, which is critical for the German export economy, it is to Washington DC he should travel, not Beijing!

The Financial Times writes, Japan and the UK are set to sign a major defence pact in December that will enable the countries to enhance co-operation with the US in the Indo-Pacific and boost deterrence against the rising threat from China. The countries will sign a Reciprocal Access Agreement (RAA). It will follow a similar deal Japan signed with Australia in January and is another sign of Tokyo forging deeper defence ties with allies and partners to prepare for the possibility of a war with China over Taiwan.

If that leaves you wondering where the US - China conflict is likely heading? According to Navy Admiral Charles Richard, the commander of U.S. Strategic Command, “This Ukraine crisis that we’re in right now, this is just the warmup”, said this week at a conference, according to the Wall Street Journal. “The big one is coming”, he also said, referring to a war over Taiwan.

Energy Transition & Technology News

Bloomberg writes, in the global race for the commodities that underpin a switch to a greener economy, China has become the dominant supplier or processor.

Shell signed an agreement with Chinese state refiner Sinopec and steel group Baowu as well as German chemical giant BASF to study a carbon capture, utilization, and storage project (CCUS) in East China, writes Reuters. Targeting not only emissions from the parties involved but also industries in the East China region, the CO2 captured could be shipped to a receiving terminal in a CO2 carrier before being transported into storage sites both onshore and offshore through short pipelines, Shell is reported to have said.

The head of decarbonisation at shipping company AP Møller-Maersk says the oil industry is holding back a clean energy transition in global supply chains. “Today, we buy our fuel from the oil companies. But they have not offered us any green methanol at a price point we can accept” he told The Financial Times. He also said the group will need about 5mn tonnes of green methanol per year by 2030 to hit its decarbonization targets, adding it may not secure this level of supply unless production accelerates. EPM notes that in addition to countries becoming more adversarial in their tone around COP27 (part of the growing rich countries versus poor countries divide we discussed in earlier daily roundups), clearly companies are starting to do the same – all to deflect blame for not delivering upon (much hyped) decarbonization targets. The oil industry should be expected to push back at the accusation with arguments along the line of “we cannot perform miracles, and with current state of technology and maturity of supply chains, the quoted prices are the best we can do for green fuels”.

Climate Politics

As COP27 in Egypt got underway, The Economist writes that the world “needs to face up to the fact” it is going to miss the totemic 1.5°C climate target. “An emissions pathway with a 50/50 chance of meeting the 1.5°C goal was only just credible at the time of Paris”, it says. “Seven intervening years of rising emissions mean such pathways are now firmly in the realm of the incredible. The collapse of civilisation might bring it about; so might a comet strike or some other highly unlikely and horrific natural perturbation. Emissions-reduction policies will not, however bravely intended.” The ultimate objective of the piece is to call for an “other, sorrier and perhaps wiser direction” of climate policy.

As to new policies, The Financial Times reports US president Joe Biden’s climate envoy John Kerry is trying to marshal support from other governments, companies and climate experts to develop a new framework for carbon credits to be sold to business. The proceeds could then fund new clean energy projects. Under the plans, regional governments or state bodies would earn carbon credits by reducing their power sector’s emissions as fossil fuel infrastructure such as coal-fired plants were cut and renewable energy increased. The credits would be certified by an independent, as-yet unspecified, accreditation body. Companies would then be able to buy the credits to offset their own carbon emissions. The FT calls the plan transformational. However, we at EPM have an alternate view on the impact because the onus and risk are placed on Government and not on commercial entities: National governments would need to take the lead in decarbonizing, through a range of subsidies for companies to make it easier for them to decarbonize. Those companies that do not want to decarbonize can then buy the rights to the resulting emissions reductions, without there being any guarantees the price of the offset will fully compensate governments for the subsidies that created them. This approach provides companies the comfortable position of “asking for subsidies to decarbonize and buying ample offsets if decarbonization is too hard work”.

The Global Energy Crisis

As you know, the current European energy crisis is the result of self-imposed sanctions policies – China and India do not have this crisis, but Europe does (neither does the US but that country is blessed with an abundance of natural resources). It is therefore critical to keep a close eye on political developments in Europe, as it is a signpost for future developments on the energy front. In that regard, The Financial Times reports tens of thousands of Italians marched through Rome on Saturday calling for a halt to arms shipments to Ukraine and a ceasefire. Members of labour unions and Catholic associations, scouts, students and a range of social activists demanded an end to fighting and a serious international diplomatic initiative to negotiate a solution to the conflict. The protest highlights the resistance that Giorgia Meloni’s new government could face, if it intends to continue the policies of the previous Italian government regarding Ukraine and Russia.

ESG

An opinion piece in Forbes highlights the origins of ESG as a tool for asset management in the financial sector. Its origins can be traced back to the formation of the UN Global Compact and a 2004 report titled “Who Cares Wins: Connecting Financial Markets to a Changing World”, which wanted to “to develop guidelines and recommendations on how to better integrate environmental, social and governance issues in asset management, securities brokerage services and associated research functions.” As such, the primary objective was to “contribute to stronger and more resilient investment markets”, with the thought being that ESG would make this translate into “sustainable development of societies”. At EPM we are of the opinion it is high time this fundamental assumption underlying the ESG movement is tested – are companies which sincerely take ESG on board really making a (noticeably) more positive difference in the societies in which they operate?