Energy, Politics & Money - 05 August 2022

Energy, Politics & Money - 05 August 2022

Curated news from the ever evolving worlds of energy, geopolitics, and money just for you!

Welcome to the Energy, Politics & Money news feed of Friday 5 August 2022, with your daily dose of cutting-edge insight into everything of importance in the connected worlds of energy, geopolitics and the economy.

In this roundup, we look at:

The impact of OPEC+’s increase in production and Russian and Saudi competition

The move to increase interest rates to combat inflation, efforts to isolate Russia falling short, and the impact of the US visit to Taiwan

How theories on Peak Oil Demand are evolving

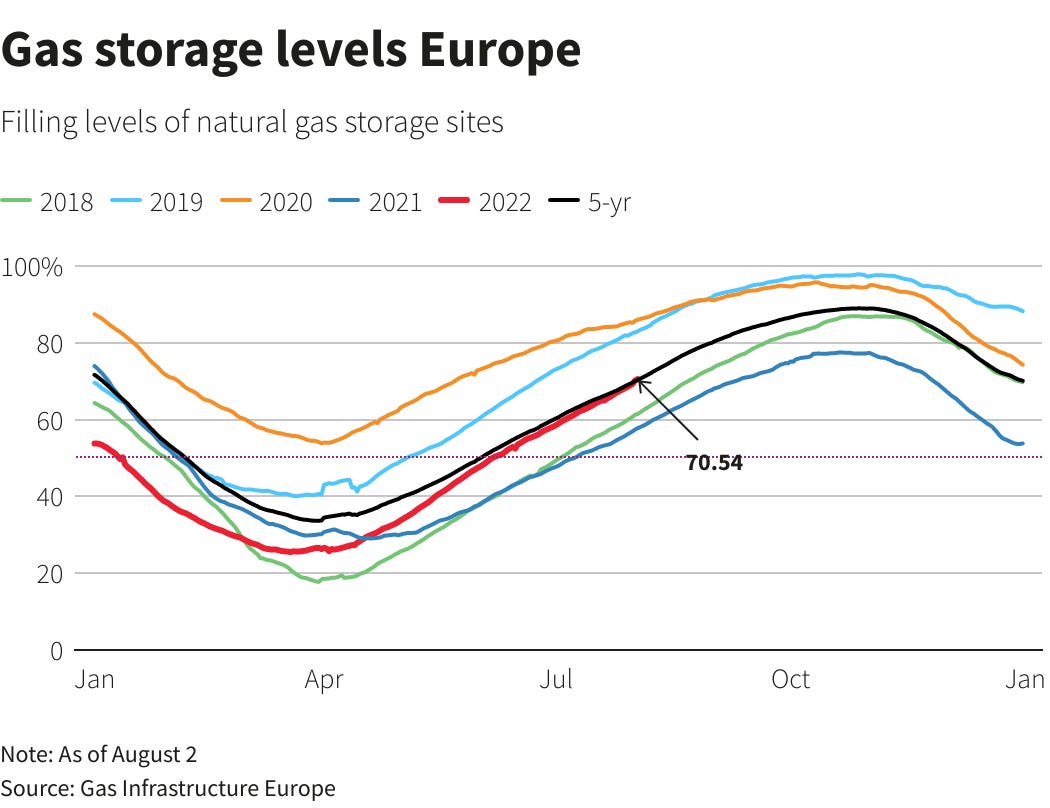

European strategic gas supply is at the 5 year average of 70%

Europe’s efforts to obtain gas are driving prices beyond what developing Asian economies can afford

The IMF advises European energy subsidies will delay the energy transition

And other gems…

General Energy News

The OPEC+ quota agreement halted the downward slide of the oil price, as it shifted the market’s focus to the supply side of the supply / demand balance, but, we’re predicting, it will be temporary. A day later, traders focused on the coming recession again, which resulted in fears around oil demand going forward and thus pushed the price down again. West Texas Intermediate traded below $89 a barrel in Asia, down almost 10% this week. The sell-off has wiped out gains triggered by Russia’s invasion of Ukraine. Bloomberg notes this will ease inflationary pressures and thus opens an opportunity for Central Banks to limit their interest rate rises.

In our analysis of the OPEC+ quota agreement, we have highlighted (starting Tuesday, before the 100,000 barrel per day increase was announced) that only countries that can significantly increase production are remain under sanctions while most other cartel members are already producing close to full capacity. OPEC+ is using these factors to justify its decision (as we reported yesterday). Reuters has further information and analysis of this narrative pushed by OPEC+ - that member countries need to save remaining unused capacity for unforeseen events in the future.

The OPEC+ agreement enabled Saudi Arabia to raise its oil price Asian for buyers to record levels. Arab Light for next month’s shipments to Asian refineries are priced $9.80 a barrel above the Middle Eastern benchmark (50 cents more than in August). According to Bloomberg they see this as a sign that the world’s largest exporter sees the region’s market remaining tight.

India is a slightly different story as there a fierce battle between brewing as Russia attempts to undercut Saudi Arabia in its attempt to expand market share. Again, according to Bloomberg Russian barrels were cheaper than Saudi crude during April through June with the discount widening to almost $19 a barrel in May. The discount of Russian oil to Saudi crude narrowed in June but the Russian barrels were still around $13 cheaper.

The Macro Environment (economics & geopolitics)

Yesterday it was the UK, today it is the Reserve Bank of India raising its benchmark rate by 50 basis points in an attempt to reign in inflation, Nikkei Asia reports. The third hike since May which leaves the rate at 5.4%.

Bloomberg has an asked a number of market analysts about their view on the main risks facing the global economy.

Geopolitically, Bloomberg reports the US efforts to isolate Russia are falling short, as half of the countries in the Group of Twenty have not signed up to the sanctions list. Economic imperatives are one reason for the resistance. But, there are other reasons as well, including historic affinities to Moscow, concerns at signs of US disengagement, and, a distrust of former colonial powers fueling a sense of hypocrisy.

Also in geopolitics, negotiations with Iran on a nuclear deal restarted yesterday. According to Bloomberg, the gulf separating Iran and the US has grown wider since the last round of nuclear talks in Vienna - as at least two new nuclear-related issues have cropped up in recent months - thereby increasing the list of hurdles that need to be cleared to six or seven.

With regards to the Pelosi visit to Taiwan, Nikkei Asia has an opinion piece by Admiral James Stavridis, the 16th Supreme Allied Commander of NATO, to share his views on the question, “If the US went to war with China, who would win?”. Our view is that a war between the US and China will not be fought (primarily) by American soldiers. It is much more likely to be fought by Japanese, Korean, Philippine and Indonesian soldiers, supplied with American weapons, intelligence and tactical support.

Nikkei Asia also interviewed Elbridge Colby, former Deputy Assistant Secretary of Defense for Strategy and Force Development under President Donald Trump. His view on the trip is neatly set out in this quote, which in typical American style includes a movie reference: “We need to shift away from symbolism and focus more on the hard work of shoring up our military position. We're like Apollo Creed in ‘Rocky IV’. We are out of shape and our opponent is Mike Tyson. We are talking smack to the press and they're hitting the gym. What matters is what happens when we get in the ring.”

Energy Transition & Technology News

Energy Intelligence carries an opinion piece that takes a step back from the daily grind to take a broader look at the subject of Peak Oil (& Gas) Demand. It highlights the fact that the strong rebound in oil demand following the Covid-19 crisis led several energy modelers to postpone the expected date of peak oil demand. For example, consultancy DNV and BP, which last year considered oil could have peaked in 2019, now see demand peaking respectively in 2024 and 2025. But, it argues, the desired and likely direction of travel has not changed.

Climate Politics

Following election of Anthony Albanese to Prime Minister in Australia, his government passed a bill to bind the country to reducing greenhouse gas emissions by 43 per cent from 2005 levels by 2030. The Financial Times reports this is seen as “a new era” of commitment to addressing climate change.

The Global Energy Crisis

Reuters reports the negotiations between Russia and Germany over the gas turbine at the heart of the Nord Stream 1 capacity utilization issue are close to deadlock. Our view that the deadlock is due fundamentally to the issue of politics. Through sanctions Europe has effectively declared economic war on Russia. They have responded to the declaration by creating an energy crisis for Europe to establish leverage for use in negotiations to reduce these sanctions. Russia’s objective is, therefore, to keep Europe “hooked” on Russian gas without giving it any sense of security. Hence, Nord Stream 1 throughput will remain at levels designed to prevent Europe from building up sufficient inventories for a comfortable winter. The turbine issue is used for cover by the Russian, i.e. “plausible deniability”.

The above explains why Gazprom has started, as reported on by S&P Global, raising concern regarding three of its turbines awaiting maintenance also face possible delays due to European sanctions.

It is key to note gas inventory levels in Europe which Reuters reports are now at 70% matching the 5-year average. This has been achieved by cutting back on gas usage, switching from gas to coal for some power plants, and increasing imports of liquefied natural gas (LNG). This is good news for Europe, but should not warrant a sense of relief or complacency. As to the sense of relief, the additional LNG imports are exceptionally expensive. For example, reaching target inventory levels is expected to cost $50 – 55 billion - around 10 times higher than normal - translating into significantly higher bills for households and industry. Furthermore, this will have far reaching consequences in the social, economic and (consequently) political realm. As to complacency, analysts and industrial experts have warned that filling up gas storage to the target levels will be impossible if Russia happens to shut off Nord Stream 1 and cut gas supplies to Germany.

Europe’s success in importing more LNG comes at the expense of Asia, highlighted by the Financial Times. This has resulted in record prices for LNG cargoes and leaves the it out of reach for many developing Asian economies and acts as a significant incentive for switching back to coal.

German companies are looking at the possibility of switching to diesel for generating power to mitigate risks of being shut out of natural gas supplies over the winter period writes Javier Blas for Bloomberg. This highlights one of our critiques of conventional risk management and business continuity approaches. Mitigation efforts are usually undertaken in isolation from the market, i.e. every organization looks at its risk and decides “I could switch to diesel to manage the issue”. By doing so, they fail to recognize that organizations all over the economy are coming up with the same idea. Consequently, when the risk materializes, risk management and business continuity plans cannot be executed. And indeed, Bloomberg also reports that OMV has halted delivery of diesel to German customers when it recognized that it was facing a run on the fuel…

Meanwhile, CNBC reports the IMF advised Europe against taking action to intervene in the energy market pricing. Instead, the IMF argues consumers should bear the brunt of higher prices to encourage energy saving and aid the wider shift to green power. The IMF said governments should strive to protect the most vulnerable households with targeted support. It notes that existing policies aimed at cushioning all consumers from rising costs will dent European economies — many already on the verge of a recession — and deter the energy transition.

Reuters also reports that the Global Energy Crisis is driving — predictably — a rethink of the role of nuclear around the world. Of course, one downside issue of nuclear is that it does not provide an immediate solution because new plant construction easily takes a decade Even a restart of previously closed sites takes months to years – just ask Germany. If anyone in energy policy were to ask us, therefore, we would not focus on nuclear for the short team (but it is a viable longer term solution).

Other

The Financial Times provides a review of the book “Oil Leaders: An Insider’s Account of Four Decades of Saudi Arabia and OPEC’s Global Energy Policy” by Ibrahim Al Muhanna. While not a “tell-all” in the western sense, it notes that Oil Leaders is an interesting window into Saudi efforts to tame whipsawing oil markets. Al Muhanna’s take is a bit light on data and it leaves readers in the dark on the all-important issue of Saudi spare production capacity. But the adviser’s revelations of governance and diplomacy are gold dust and run far deeper than the 2016 memoirs of his former boss Al-Naimi.