Energy, Geopolitics & Money - 2024.02.15

Energy, Geopolitics & Money - 2024.02.15

Non-partisan, objective & neutral analysis where global developments in energy, business & geopolitics intersect & curated from leading global sources & resources.

Welcome to EPM, where we take our daily look at the interconnected worlds of Energy, (Geo)Politics and Money. Curated from the world’s leading sources of information, we provide you both the information and the fact-based, politically-neutral commentary that you need to make sense of it all – and beat the market.

In this roundup, we look at:

The oil companies’ focus on new low-cost fields, which indicates a strategic belief that prices are unlikely to increase, driven by demand

Shell’s belief that LNG demand will continue to grow, to reach 625-685 million metric tons per year in 2040, 50% higher than today

The rousing of investor sentiment in the US, as expectations that the Fed would declare victory over inflation and quickly pivot to cutting rates are on the retreat, raising the possibility of a selloff in the stock and bonds market in 2024; where EM explains the two sides in the debate on interest rate cuts

Continued tensions on the border between Israel and Lebanon, and why the US positioning in the current Middle East crisis is likely to cause irreversible damage to its reputation in the Middle East region

Germany’s performance in its “Zeitenwende”, that is the rebuilding of its military to make it ready and capable to wage war again

Europe’s doubling down on nuclear energy, to decarbonize its electricity sector post 2040

The renewed urgency among investors to work out the implications of Scope 3 emissions disclosure for the companies they invest in, as the EU, US, UK and Japan consider mandatory disclosure of these emissions by corporations

General Energy News

Oil majors are targeting new oilfields that can be profitable even if oil prices fall to about $30 per barrel, writes Reuters. Exxon, Chevron and Occidental recently struck deals worth a combined $125 billion to acquire companies that will help them pump oil for between $25 and $30 per barrel. In Europe, Shell and Equinor are pursuing projects with $25-30 per barrel breakevens, while France’s TotalEnergies aims to get its production costs under $25. What this indicates, Reuters says, is that unlike at previous moments in history, the majors are now not expecting a demand driving increase in oil prices, but rather another crash. "After three major oil price crashes in 15 years, there is wide acceptance that another one is likely to happen," it quotes Wood Mackenzie as saying. New production tends to be highly prolific deepwater fields, where platforms turn into cash machines once paid off, or shale, where a collection of small and easy-to-tap wells allows for adjusting volumes depending on energy prices.

Where many oil majors do see an increase in demand, is LNG. Shell expects it to rise by more than 50% by 2040, Reuters writes, as China and countries in South and Southeast Asia use LNG to support their economic growth. Demand for natural gas is expected to reach around 625-685 million metric tons per year in 2040, Shell says. That is slightly lower than Shell's 2023 estimates of a global demand increase to 700 million tons by 2040. Demand has peaked in some regions, including Europe, Japan and Australia in the 2010s, but continues to rise globally, is Shell’s belief.

Macroeconomics

Expectations that the Fed could declare victory over inflation and quickly pivot to cutting rates was a key driver behind last year's stellar 24% gain for the S&P 500, writes Axios. But belief that the Fed will reduce rates again starting in March has dwindled since. The Fed funds futures market indicated that in 2022 the odds for a Fed rate reduction in March stood at 90%. Today, they stand at 9%. The odds for a rate reduction in May still stand at 60%, but they are declining by the day. Axios believes that if the rate cuts are put off much longer investors may start to offload their 2023 investment, driving the stock makret down again.

An opinion piece in the Financial Times explains the thinking on the different sides of the equation. Those calling for “Fed caution” are of the view that the inflation of recent years was due to an overheated economy (in no small part due to US government spending programs). They rely on a piece of economic modeling known as the Phillips curve that says to get inflation down, unemployment must rise. This faction of observers and analysts wants a tight monetary policy with high interest rates to slow the economy down into recession, as this will increase unemployment and push down prices. On the other hand, there are those who believe the increase in inflation was due to supply chain bottlenecks caused by Covid-19 pandemic. This faction of observers and analysts fears the Fed’s high interest rates because it causes a recession – which they believe is not necessary to bring inflation down since it is not demand but supply caused.

Geopolitics

Tensions remain high on the border between Israel and Lebanon, writes the Financial Times. On Wednesday, Hezbollah struck an Israeli military base in Safed, about 20km from the border. One soldier was killed and eight others injured. In retaliation, Israel then bombed residential areas in Southern Lebanon, killing at least 9 civilians, four women and four children. Hizbollah said three of its fighters were killed in separate Israeli airstrikes.

The US finds itself in the last place it wanted to be in the Middle East, writes Bloomberg. Its main ally, Israel, isn’t listening to it, with Prime Minister Netanyahu not heeding President Biden’s pleas to do more to limit the number of civilians killed in airstrikes and to move toward another cease-fire. The US is also now facing an enemy it never wanted to take on. Groups backed by Iran have seized the moment of chaos, carrying out a record number of attacks on US and allied military assets in the past month. Even if Biden and his allies manage to maintain or even reduce the current level of tension, actions—or instances of inaction—by the US will have ripple effects. The Iraq War and the Arab Spring are two examples of previous moments in which many in the Arab world say the US stood on the wrong side of history. Its current positioning in the War on Gaza could make the damage to its reputation in the Middle East region irreversible this time.

The above is a view that EPM has previously articulated as well. In fact, we see possible outcome as so extremely likely, that we do not fully comprehend why the US has taken its one-sided stance in the broader Middle Eastern conflict at present. Perhaps it is because it is being advised by people who have ulterior motives, such as Kenneth Pollack, senior fellow at the American Enterprise Institute, former research director at the Saban Center for Middle East Policy, and once accused of espionage in support of the American Israel Public Affairs Committee (AIPAC). According to S&P Global, Pollack told members of the US House of Representatives that the best way of dealing with the Houthi threat to shipping across the Red Sea is by supporting local and regional efforts to retake Houthi territory – in other words, EPM notes, by starting another war in Yemen. It does not mean there should be American boots on the ground in Yemen, Pollack said. But it will ultimately require the US to arm, equip and train the anti-Houthi coalition operating under the umbrella of the government of Yemen, and it could require employing American air power as well, he said. In the EP view, the last thing the US needs is more war in the Middle East. Over the past three decades, this approach to geopolitics has brought it nothing but financial loss and erosion of both its soft power and hard military force.

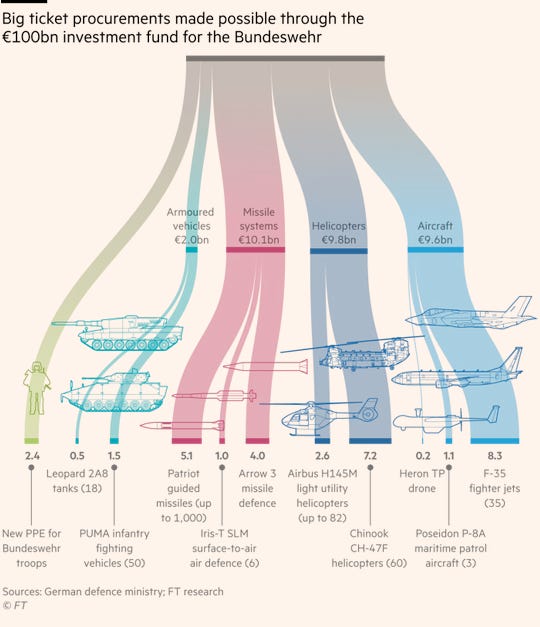

The Munich Security Conference, the “Davos of Defence”, opens this week, and the Financial Times looks at Germany’s performance in its “Zeitenwende”. Just three days after Russia embarked on its full-scale invasion of Ukraine, Chancellor Olaf Scholz announced a cash injection into the German military of €100bn from a Special Fund, as well as a structural increase in defence expenditure to meet NATO’s “2% of annual GDP” target. Germany will spend nearly €72bn on defence in 2024, more than it has ever done in the history of the Bundeswehr, and a clear indication of German willpower to deliver upon the promise. Some €52bn will come from the regular budget and €19.8bn from the fund. But concern is growing about what will happen after 2027, when the fund has dried up. Experts believe the country will then have to stump up an additional €25bn-€30bn a year out of the general budget to meet the 2 per cent goal — an eye-watering sum that could require swinging cuts in welfare spending if the country is to balance the books. The political support is there. All three parties in the government, as well as the opposition Christian Democrats (CDU) and its Bavarian sister party, the CSU, are committed to the 2 per cent goal. But no one in politics knows how to achieve it, and is fearful of a voter’s backlash. Additionally, defense specialists argue that the 2% target is not sufficient to establish a Bundeswehr that is, in the words of Germany’s defence minister Boris Pistorius, “kriegstüchtig” — a word that means “ready to wage war and capable of doing so”.

Climate Politics

Details of a "European Industrial Alliance on SMRs" have been announced, writes S&P Global. "As we are facing a race to generate sufficient decarbonised electricity to achieve our climate ambition, nuclear energy, and Small Modular Reactors (SMRs) in particular, has a central role to play," Thierry Breton, EU commissioner for the internal market, said in a related statement.

This EU focus on nuclear in general, and SMRs in particular will surprise many, as it comes not long after the Hickley debacle in the UK, where costs have overrun by the tens of billions and delays run in the years – a common occurrence in the nuclear industry. Energy Intelligence has an article that sets out the view that nuclear – conventional or SMR – should not be considered at all in the decarbonization debate.

Other

Regulators from the European Union, Japan, the UK and elsewhere have signaled that mandatory Scope 3 emissions disclosures are on the horizon for corporations. The US Securities and Exchange Commission has also discussed whether big emitters should be required to disclose their Scope 3 emissions. As a result, Bloomberg writes, there is now a renewed urgency among investors to work out the implications of Scope 3 emissions disclosure for the companies they invest in. Just 45% of the 4,000 medium to large-sized publicly traded companies disclose Scope 3 data. And even when the data does exist, making it useful for investment purposes is another matter entirely. Unlike Scope 1 and 2 emissions, which are derived from a company’s own activity and from purchased energy, accurately assessing Scope 3 is much more difficult. The GHG Protocol divides Scope 3 into a whopping 15 categories, ranging from the emissions resulting from purchased goods and services, to business travel and the processing of sold products.